Overview

We all are surrounded by different uncertainties and risks in our life. Whether a celebrity or a normal human being; everyone lives in the fear of losing valuables. People have different worries like health issues, financial loss in business, death loss, job insecurity, etc. Apart from these worries, another fear is related to property loss and natural calamities i.e. earthquake, floods, famine, fire, drought, etc. In organizations also, both employees and employers are worried about different risks, like employees have a risk factor of losing jobs and employers for the wellbeing and physical safety of employees. So, we can say that everybody experiences risks and uncertainties at some point in their life.

Insurance offers a way to provide protection from above different financial losses. It is considered as one of the mediums for providing not only financial security but also emotional and materialistic security. Insurance supports by protecting us from uncertain possible risks i.e. accident, fire, sudden death, major health-issues, burglary, etc. Insurance can be broadly classified as Life Insurance and General Insurance.

• Life Insurance: It is considered as a contract that provides compensation in monetary terms in case of disability or death of a person. Even a few life insurance policies are composed to provide post-retirement financial security or for a fixed period. We borrow life insurance policy by making a lump-sum payment or periodic payments i.e. Premium to an entity that provides insurance i.e. “Insurer or Insurance Company”. In lieu of the premium, the insurer or insurance company assures to compensate an assured amount to the family in case of disability or death or at a defined time.

So, we can say that life insurance secures families by providing financial security even in the sudden death of a family member.

• General Insurance: It is a contract that provides financial security in the form of compensation on other losses except for death. These financial losses can be related to different liabilities like travel, health, vehicle, house, etc. Through this, insurance companies are liable to pay a sum assured of the compensation that covers vehicle damage, financial loss at the time of travel, medical expenses while taking treatment on health issues, financial loss due to fire or theft or natural disasters, etc. General Insurance is mainly of 5 types i.e., Health insurance, Vehicle insurance, Travel insurance, Home insurance, and Fire insurance.

A Brief Background

The evolution of the Insurance concept and Insurance business happened long back when businessmen throughout the world used to travel from one nation to another for business and trade purposes. The primary and cheapest way of transport was to utilize waterways. Boats and ships were the transport medium for shipping stock and inventories. But often boats containing cargo were drowned or stolen by pirates or lost.

So a group of 10 merchants or businessmen looked for a solution for bearing risk due to the above loss of inventory and boats. As a solution, each of them contributed 10% worth of inventory or stocks, and the same was collected in a bag. After the contribution of each business member, the bag had enough money to compensate any ship owner who lost his ship to prevent any financial or mental loss. So, this act of these merchants is considered as commercial insurance in which they were insuring the risk on a mutual basis by money pooling (premium) and further providing that money as compensation to the merchant who suffered the loss (sum assured).

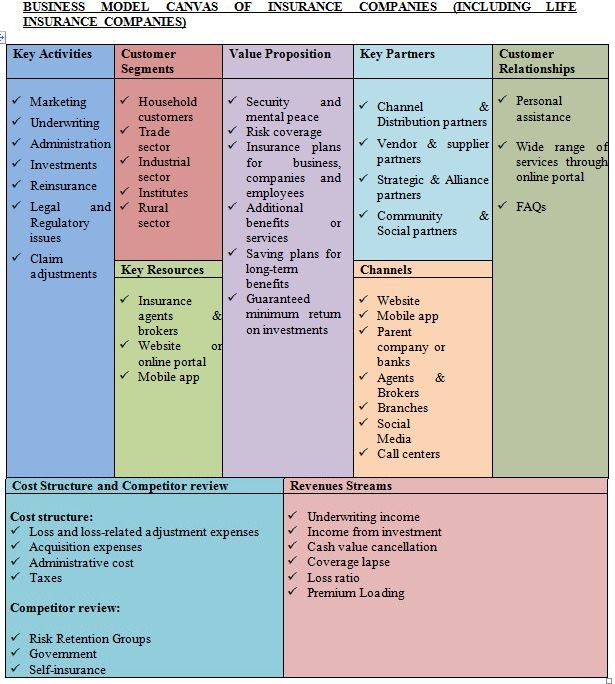

Business Model of Insurance Companies

The business model of an Insurance company involves an agreement or contract between the insurance company (insurer) and people who are insured (customer or insurance policyholder). The base of the business model of insurance companies revolves around prediction and diversification of risk. It is a risk-sharing model in which risk is pooled from individuals and redistributed among a large group of people. Before discussing the business model of Insurance companies in detail, let’s first have a look at the “Working mechanism of Insurance business”.

Business Model Canvas of Insurance Companies (Including Life Insurance Companies)

Different elements mentioned in the above business model canvas of Insurance Companies are as under:

A) Value Proposition

Following is the value proposition of insurance companies.

- Insurance companies provide different insurance policies to cover various unforeseen events to enable businesses and individuals to disburse their daily activities smoothly. These policies remove the future possibility of any big and unaffordable potential loss by providing security and mental peace. Also, losses of the few people are distributed among many.

- Different insurance policies are offered by insurance companies to cover various types of risks like home insurance, life insurance, vehicle insurance, health insurance, etc.

- Businesses and companies can also take benefits of various insurance plans like Worker’s compensation, Property insurance, Group mediclaim, Group personal accident insurance, Fire insurance, etc. to save the interest of their employees and business assets in hard times or unexpected losses.

- Insurance companies cover risks of customers against old age, death, illness, disability, etc. They provide various additional benefits or services along with core insurance products aimed at risk prevention, fast handling of claims, etc. This also includes providing health advice or cyber-security advice.

- Insurers offer various saving plans for long-term benefits, like pensions. The products offered by the insurance companies are mostly the combination of investment and protection against different risks. Thus, customers get the advantage of both returns on investment and life risk cover.

- The products of Insurance companies have guaranteed minimum returns. So, it ensures people, that their savings are safe. Even in fluctuations in stock markets, customers will still get the money as agreed at the defined time.

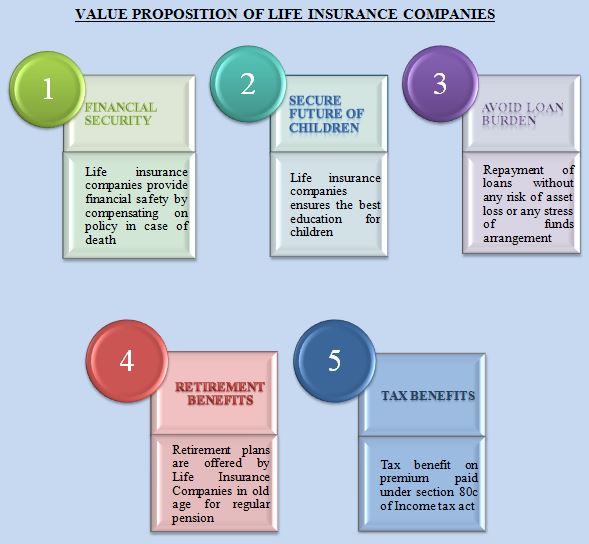

Value Proposition Especially Offered by Life Insurance Companies

The chart depicts the value proposition offered by life insurance companies

- Financial Security (peace of mind):

– In case of death: Life insurance companies offer great peace of mind by ensuring financial safety to the family in case of demise of life insurance policyholder.

– In case of health issues or major disease/illness: The major part of the income of Indians is used in healthcare and medicines. There are great chances of no earning or income during treatment in case of suffering from a critical or major illness. Life insurance companies play a significant role during this time by providing financial protection to fulfill family needs, medicine, and treatment needs.

For example, ICICI Prudential life insurance has an ICICI Pru iProtect Smart Plan that includes ICICI Prudential smart health cover for the critical illness of worth Rs. 10 lakh cover and for 15 years.

- Secure future of children: Life insurance companies encourage savings or funds for the education of children. A child insurance plan is there to fulfill educational needs of children. These policies generally come under ULIP (Unit linked insurance plan) that facilitates the increase in investments and educational support. Such as, a parent at the age of 35 years takes a 15-year child insurance plan with Rs. 10 lakh sum assured and saves Rs. 1 lakh on annual basis for the purpose of higher education of a child. In case of unfortunate death of the parent at the age of 40, Rs. 10 lakh amount will be handed over to the child for fulfilling the requirement of immediate educational cost.

For example, ICICI prudential life insurance has ICICI Pru Smart Life plan that gives the additional benefit of waiving off the remaining premium amount in case of death of parent that also without intact of financial protection cover.

- Avoiding loan burden by wealth creation: Life insurance companies also offer few life insurance plans that provide the medium for wealth creation. These plans or policies provide benefits of life cover and great returns by investing the premium of policyholders in various beneficial investment categories. This helps in minimizing the burden of taking and repaying loan for financial needs by encouraging savings and enhancing wealth. For example, ICICI Pru Signature which is a ULIP plan of ICICI Prudential life insurance offers such benefits.

- Retirement benefits: In the old age, everyone wants to be free from all financial burdens and work pressures to enjoy the retirement period. This can be peaceful if there is a stable monthly income or pension. As more people are working in private sectors where pension benefit is not available or very rare, so retirement seems like a burden or pressure. To avoid such worries on retirement, life insurance companies offers retirement plans through which retired people are able to get a pension and can live their life without being financially dependable on others. These retirement plans provide regular pension to a retired person and his/her spouse. For example, if a 60 years old person buys ICICI Pru retirement plan i.e. Immediate Annuity-retirement plan of Rs. 1 crore then he/she can receive Rs. 61k per month as retirement pension for the rest of the life.

- Tax benefit through tax savings: Tax benefits are also offered in Life insurance plans by insurance companies. The premium paid by the policyholder comes under the tax deduction of section 80C in the Income Tax act. So, up to Rs. 1.5 lakh annual premium is a deductible amount from gross income that lowers the tax outgo. Moreover, the maturity insurance plans are totally tax-free.

B) Customer Segments

Different customers of Insurance companies (including life insurance companies) are

- Household customer segment: This includes self-employed people, retired employees, and salaried class customers

- Trade sector: Different small and large businesses are included in this

- Industrial sector: Both public and private industries are also customers of Insurance companies

- Institutes: Various universities, schools, colleges, and institutes fall in this customer segment

- Rural sector: This segment is categorized as per age i.e. kids, youth, old age, etc. and gender-wise segment i.e. Men and Women.

C) Key Partners

The key partners of insurance companies are:

- Life Insurance and general insurance companies have network partner companies to support them in their different operational activities. The key partners of insurance companies are categorized as below:

Channel and distribution partners: This includes third party intermediaries of insurance companies like agents, brokers, banks, independent consultants that work on the behalf of insurance companies in providing products and services of them and also, expand the market reach of insurance companies. Different banks and insurance companies have a partnership for selling insurance products of insurance companies to clients of banks. This partnership is termed as Bancassurance.

- Vendor and suppliers as partners: This includes suppliers of technologies, services, equipment to support the main operations of insurance companies. For example, ICICI Prudential Life Insurance has tie-up with Paytm for marketing and selling its product i.e. ICICI Pru iProtect Smart (a protection product) using the Paytm app. Similarly, the company is in partnership with Airtel Payment Bank to provide easy and fast access to savings and life insurance plans of ICICI Prudential to the customers of Airtel Payment Bank.

- Strategic and Alliance partners: This includes different companies that have a tie-up with insurance companies for projects related to the marketing and branding of insurance companies.

- Community and Social partners: Various charitable and non-profit organizations are partners of insurance companies for community and social projects.

D) Key Resources

These are the key resources of insurance of insurance companies.

- Insurance agents and brokers: The insurance agents and brokers are the main resources of Insurance companies, especially life insurance. These are the 1st point of contact for customers who are looking for insurance. These agents and brokers facilitate customers in selecting the best insurance cover by providing all necessary information. Insurance agents usually work for a particular insurance company and sell the insurance products of that company only. Wherein, insurance brokers serve customers who are looking for insurance and so these brokers are associated with multiple insurance companies to sell their products.

- Online portal or Website: Insurance companies have their own website that contains all necessary information about their products and services for different types of customers according to their needs. People can apply directly to these websites for insurance cover. Also, customers can apply through the website of Insurance agents, brokers, and third parties.

- Mobile App: Various life insurance companies have their own mobile app to facilitate customers with quick and easy apply, access for insurance, and related services. For example, ICICI Prudential Life Insurance has a mobile and tablet app i.e. ICICI PruLife for the purpose of online sourcing and servicing of life insurance policies. Customers, Advisors, Employees, and Sales Partners of the company can access and use the app.

E) Key Activities

The main activities of Insurance companies are as below:

- Marketing: This includes primarily marketing activities like advertisement and promotion of insurance-related products and services. Different agents and Brokers are the sources to sell and advertise most of life or health insurance policies. All big groups in the insurance sector have their own websites for promoting the product features of insurance companies.

- Underwriting: Insurance companies are involved in underwriting which is the process of categorizing the potential insurance policyholders into the applicable risk classification. The purpose of underwriting is to charge the appropriate price or rate.

- Administration: Insurance companies do various administrative activities once the insurance policy is sold out and underwriter approves it like establishing records, collecting premiums, answering queries of customers, and various other administrative jobs. Administration includes management of various other functions i.e. accounting, customer service, information systems, personnel management, and office administration.

- Investments: Different Insurance companies have their own investment firms (e.g. mutual funds firms) that perform tasks related to investing the premium in the capital market in order to gain the best ROI (return on investment) for providing security to policyholders.

- Reinsurance: Insurance companies are also involved in reinsurance activities through which they transfers either complete or a part of its risk to another insurance company under an insurance contract.

- Legal and Regulatory Issues: Insurance companies have lawyers who are involved in various legal activities like drafting insurance contracts, interpreting provision of contracts at the time of presenting claims, defending the insurance company in lawsuits, communication with regulators, etc.

- Claims adjustment activities: This includes activities related to providing payment to insured customers on losses.

F) Channels

These are the channels of insurance companies.

- Websites: Insurance companies have websites that display information related to their products, services, and other activities. The website of the insurance company provides an online medium for making online payment of premium, getting insurance proof, filing a claim and to monitor its progress, etc. It includes detail of various policies that an insurance company offers to its customers along with specific provisions.

- Mobile App: Insurance companies also have a mobile app using which customers can access the information related to their policy, file a claim, and can track their progress, etc.

- Parent company or Banks: Few of the Insurance companies have their own banks as a parent channel for initiating insurance activities like HDFC Life Insurance has its parent company i.e. HDFC Bank.

- Individual agents and brokers: Insurance companies sell and promote various insurance products and services through the channel network of brokers and agents. For this, insurance companies provide a commission to them.

- Branches: Insurance companies have different branches at different locations of the country which acts as a channel for insurance business activities. These branches also sell and promote insurance products directly other than brokers or agents.

- Social media: Social media like Facebook, Linkedin, Twitter, Whatsapp, etc. are also key channels of Insurance companies where they advertise and promote their products and services to generate sales.

- Call centres: Various insurance companies take services of call centers of BPOs for selling and promoting their insurance products.

G) Customer Relationship

The insurance companies offer the following customer services.

- Insurance companies provide a wide range of services to its customers for superior customer relations. Through the online portal or websites of these companies, customers can manage various activities like bill payments, account information, access of resources, and claim submission directly without any hassle of interacting with sales or service representatives.

- Insurance companies offer continuous support to customers by providing various online resources such as answering FAQs (frequently asked questions) and guides, direct customer support assistance through the dedicated support and service staff of the insurance companies to provide guidance and resolve queries via email or over the phone call.

H) Revenue Streams

The main resource of revenue/income of Insurance companies (including life insurance) is the premium paid by people who have purchased insurance. These premiums can be lump-sum i.e. all payment at once or in instalments or regular intervals i.e. monthly, quarterly, annually, etc.

Other than charging premiums for insurance coverage, insurance companies also reinvest these premium amounts in other assets that generate interest income.

I) Cost structure and Competitor Review

Costing

Different costs that revenue of Insurance Company (including Life Insurance Company) covers are as under:

- Losses and loss-related adjustment expenses: A life insurance company keeps a portion of its reserves for unpredictable future losses, investigation cost, and loss adjustment costs. These reserves are kept by estimating the losses an insurance company may experience in the future. Loss adjustment cost or expense is the cost bore by the insurance company during the settlement of claims. So, they have claim representatives who investigate claimed losses. As the company has to pay them for the services, so these expenses come under loss-related adjustment expenses.

- Acquisition cost: These expenses mainly include marketing-related costs, like advertisements, commissions of insurance agents and brokers, etc.

- Administrative expenses: These are considered fixed costs like office equipment and computers, etc.

- Taxes: Insurance companies are also liable to pay taxes and are considered as expenses.

Competitor Review

- Insurance companies compete with risk retention groups, government, and also, self-insurance. The government mostly facilitates insurance cover for risks like floods, earthquakes, etc. States also provide insurance in few places like Employee state insurance (ESI), Worker’s compensation, etc.

- Different RRGs (Risk retention groups) are also competitors of Insurance companies that provide coverage for specific liability risks like malpractice in medical.

- Different large organizations or businesses that self-insure for employee benefits like health coverage; are also considered as competitors of insurance companies.

Revenue Model of Life Insurance Companies

Let’s have a look in detail that how life insurance companies generate revenue:

- Income from Underwriting: Underwriting revenues are those that are derived from subtracting the amount paid out for claims/final settlement from the actual amount that life insurance companies collect through premiums by selling insurance policies. For example, in a particular year, a life insurance company earned revenue of Rs. 1 Crore through premiums by customers for insurance policies. It further paid Rs. 50 Lakh as settlement amount or claims. So, we can say that the profit earned by the company i.e., Rs. 50 Lakh (1 crore-50 lakh) would be underwriting income for that year.

- Income from Investment: Lots of money is being earned by life insurance and general insurance companies through investment income. The premium amount paid by insurance customers is collected and invested in financial markets by insurance companies. Generally, the amount is invested in stocks, bonds, different other businesses, and in other insurance companies as well under few circumstances. So, the residual income generated from investing the premium amount in capital or financial markets is considered as income earned from investment. Life insurance companies prefer to invest the premium amount to gain the advantage of returns rather than keeping the money in idle stage until they receive actual claims for settlement. The insurance companies invest money in both low and high-risk investment mediums, like investing in securities of fixed income at lower risk and investing in equity markets to gain appropriate returns. For example, HDFC Life Insurance has various ULIP (Unit linked insurance plan) investment plans for customers for better returns like HDFC Life Click2 Wealth, HDFC Life Sanchay plus, HDFC Life Sanchay Par Advantage, etc.

- Cancellations of cash value: As life insurance companies invest the premium amount of policyholders, so the customers who have whole life insurance policy demand for the cash values or money that is earned by dividends and investment from the investment plans of life insurance companies. For this, even they also prefer to close or surrender their life insurance policy. This provides an opportunity to earn profit to the insurance companies as all the liabilities of their side ends once the cash value of money is paid to customers. By keeping the entire already paid premium amount, insurance companies provide interest income to customers on their investments and remaining cash they keep with them. So, cash value payouts are considered as a financial windfall for life insurance companies.

- Lapse of coverage: When customers are unable to pay the premium amount or miss the premium payment then it is considered a life insurance policy lapse which is a profitable part for insurance companies. In this scenario, the life insurance companies are not liable to pay any claim or death benefit or give insurance coverage to the insured customer. This is one of the jackpots for insurance companies as they keep the entire previous paid premium.

- Loss Ratio: Insurance companies use different statistical tools to take an estimate of the final claim ratio for a specific year. This ratio is termed as loss ratio which includes both reserved, paid total losses, and all operating expenses. For example, let’s say Rs. 60 is paid by a life insurance company in settlement of claims against the collected premium of every Rs. 100; the loss ratio is 60% and the profit ratio is 40%. This 40% profit ratio is included in some expenses i.e. operating costs of the company and the rest part of it will be considered as the net profit of the insurance company.

- Premium loading: Life insurance companies also make a profit or extra income through premium loading. Some Insurance policyholders are considered as high-risk customers like customers into risky work i.e. Army, Pilot, Air Force, etc. or people suffering from critical diseases or chain smokers or drinkers, etc. In such cases, insurance companies may raise the premium for policyholders, and this increased premium is considered as premium loading.

Summary

Insurance plays a significant role in the economy of India and other countries. It supports the economic activities of the country by assisting people and businesses to cope with their risks. The business model of insurance companies facilitates organizations to focus on their business functions and effective utilization of resources.

Insurers earn revenue mainly through underwriting income and investment income. Most of the assets of insurance companies are financial investments, mainly listed shares, government bonds, commercial property, and corporate bonds.