Overview

Credit Cards

Credit cards are considered as one of the most beneficial sources for making purchases. It allows us to borrow money from a financial institution like a bank for the purpose of buying things like household things, travel tickets, hotel bookings, and many more. Both cost (fees and interest charges) and benefits (credit score and reward points) are associated with credit cards. A credit card is a metal or plastic made rectangular slab that a financial company issues to its customers. It allows cardholders (customers who have credit cards) to borrow money with a condition to pay back the money and any additional interest or fee as per terms & conditions. Banks and other financial institutions issue credit cards of different companies like Visa, Discover, American Express, MasterCard, etc. The use of a credit card is convenient and safe while travelling or going outside for shopping purposes, as it is unsafe to carry a lot of cash to a public place. It encourages cashless transactions for different purchases.

Credit Card Companies

From a broader perspective, Credit card companies consist of 2 types of setups i.e. Issuers and Payment Networks. Issuers are banks and credit unions that provide credit cards to customers such as HDFC Bank, ICICI Bank, and SBI Bank. The credit card transactions are processed by Payment Network companies, like VISA, MasterCard, American Express, etc.

A Brief Background

The U.S. is the country that initiated the use of credit cards in the 1920s. At that time different firms like hotel chains, oil companies, etc. started issuing these cards to their customers for any purchase made at the outlets of these companies. The first credit card at the universal level was launched by Diners’ Club, Inc., in the year 1950. Another card of similar type was issued by American Express in 1958, and it was a travel and entertainment card. Later, the credit card system of banks was innovated through which the merchant’s account is credited by the bank after receiving sales slips and the bill is generated to the cardholder at the end of the period. The bank of America, California started state-wide first national plan i.e. BankAmericard, which was renamed VISA during 1976-77.

Business Model OF Credit Card Companies

Before understanding the Business model elements of credit card companies, we need to be familiar with different parties involved in the transaction of a credit card. Let’s have a look at these.

- Cardholder: The credit card is owned by the customer who uses it for payment purpose at the time of purchasing anything.

- Merchant: The credit card payment is accepted and processed by the business owner i.e. Merchant who sells goods or services to customers.

- Issuing Bank: The organization that provides Credit cards to different customers like banks i.e. HDFC, ICICI, SBI, Citibank, etc. and are members of card associations. Issuing banks make payments to acquiring banks for purchases made by their cardholders. As per the credit card agreement, the cardholder becomes liable to pay back the money. Non-payment liability is shared by acquiring bank and issuing bank as per the rules & regulations laid down by the card association.

- Acquiring Bank: This is known as the merchant’s bank, as their dealing is with merchants, and they are liable to make payments to the merchant. Acquiring banks send a request to merchants for the acceptance of their card. They hold the funds of merchant and acquire the funds once the sale is made after credit card’s authorization and further they deposit these funds into the account of merchant’s bank.

- Payment Network: These are the organizations that are responsible for processing credit card related transactions. Different payment network companies like MasterCard, Visa, American Express, Discover, etc. act as a link between issuing and acquiring banks. These banks have tie-ups with a payment network to fulfil the credit card payment requirements. This facilitates the use of a card issued by an Indian bank in other countries for purchasing, and for this, a direct relationship between banks is not required.

- Processor: The credit card processors are those companies that not only collect the information but also route the data across to different stages, and supports communications among different parties. The chief role of the processor is to provide the information related to the payment to the card network.

Let’s understand the above parties involved in the credit card process with an example. Mr John (cardholder) visited an electronic showroom (merchant) to purchase an air conditioner. He made payment through HDFC Bank credit card by swiping the card on the ICICI Bank’s provided EDC (Electronic Data Capture) machine. After the successful authorization after swiping and entering his credit card PIN, Mr John receives a payment confirmation message on his registered mobile number for charging the amount from his HDFC credit card.

Different parties involved in the credit card payment process in the above example are:

- Cardholder: Mr John

- Merchant: electronic showroom

- Card Issuing bank: HDFC Bank

- Card Acquiring bank: ICICI Bank

- Payment Network: MasterCard

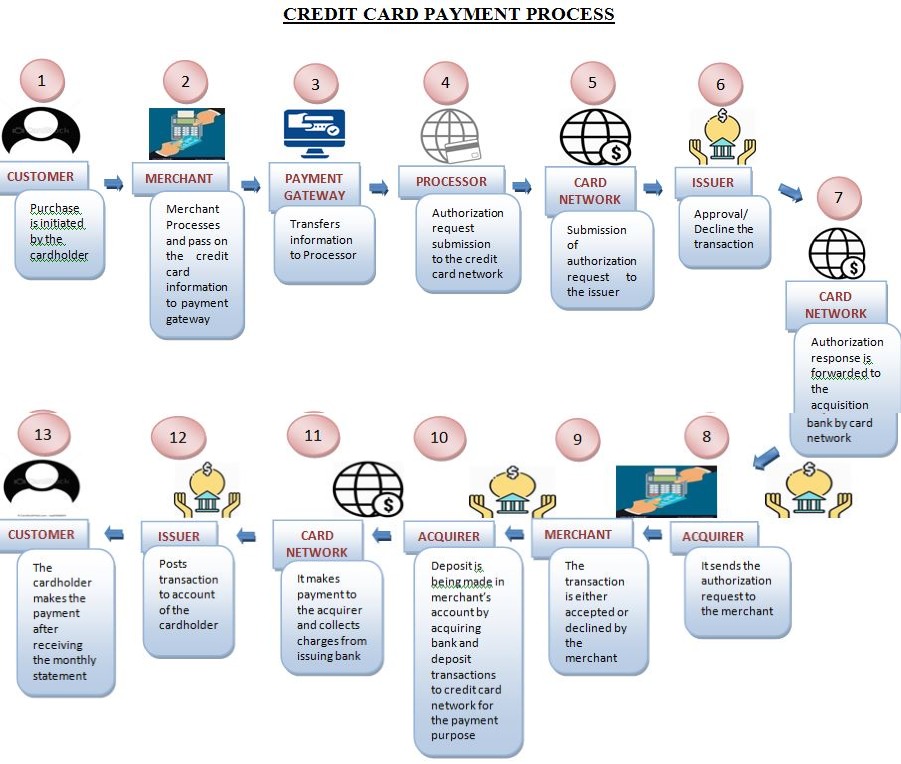

Credit Card Payment Process

The process of credit card payment is explained in the below flow chart:

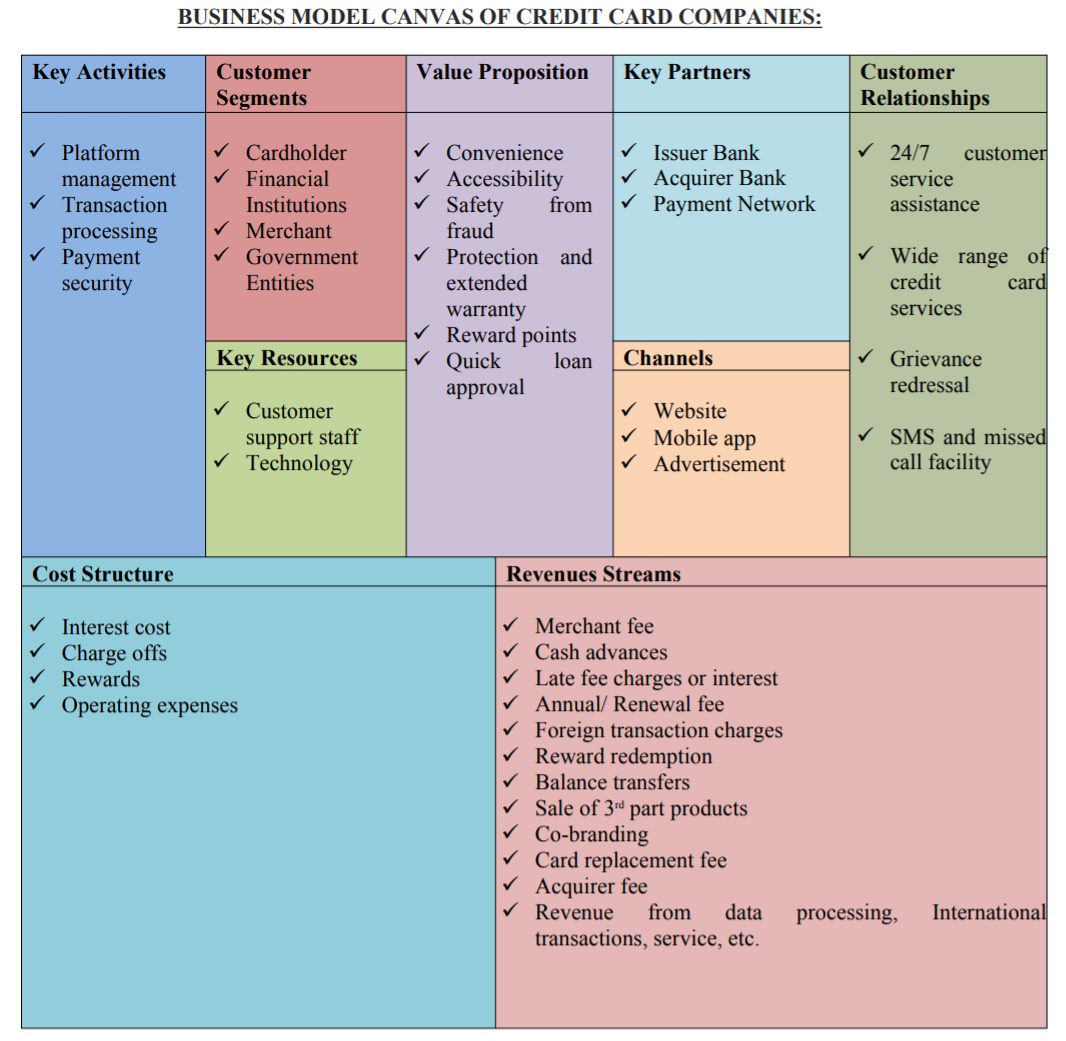

Business Model Canvas of Credit Card Companies

Different elements mentioned in the above business model canvas of Credit Card Companies are as under:

1. Value Proposition

Various unique features or benefits are offered by credit card companies to its customers, i.e.:

- Convenience: The credit card companies make life easier as it is very convenient to borrow money from their bank accounts and there is no need to visit their branches physically. Just by using ATMs, without having any handy cash, customers can pay merchants for any purchase.

- Accessibility: Credit card companies increase accessibility by providing different types of credit cards for different purposes.

- Security against fraud or unfair activities: Credit card companies have expertise in handling fraudulent activities as they create a series of defence between the customer’s money and fraudsters. Almost in every case, customers are not responsible for an unauthorized transaction of their credit card amount. And also, it doesn’t affect the bank account. Moreover, in case of customers encounter any problem with the purchase made at a Merchant shop and the Merchant refuses to pay a refund, then customers have the option to inform their credit card company to reverse the amount paid.

- Protections and extended warranties: Many credit card companies facilitate customers through purchase protection in which banks provide replacement of the damaged product purchased from Merchant, which cannot be covered in the warranty. Few credit card companies also provide price protection on purchase into which the bank refunds the difference of price in case of reducing the product’s price by a store within a certain time limit after the customer purchases it.

- Reward on credit card payments: Most of the credit card companies provide reward points while making transactions through credit cards. Customers can redeem these reward points on vouchers, gifts, etc. Also, few card companies provide facilities of special cards having accelerated reward points once these cards are used for specific transactions like dining, online shopping, flight booking, etc.

- Faster Loan Approval: Credit card companies also help customers in availing loans easily. Customers who have a good credit score i.e. they pay their due credit card amount timely, can attain loans much faster.

2. Customer Segments

These are the customer segments of credit card companies.

- Cardholders: Different customer segments like college students, corporate employees, business owners, startups, etc. are the main cardholders and customers of credit card companies.

- Financial Institutions (Issuer and Acquirer): For Payment Network companies like VISA, MasterCard, both Issuing bank and Acquiring bank are their primary customers. A huge range of branded payment products related platforms are offered by VISA company to the issuing banks which these banks utilize for developing and offering prepaid, credit, and cash access programs for their credit card customers i.e. businesses, individuals, and government entities.

- Merchants: This includes businesses or shopkeepers who are into trade or commodity business. They take payment from customers for purchase through credit cards and transfer it to the acquirer for processing.

- Government entities: Different government organizations take services of credit card companies for processing electronic payment transactions like payment of electricity bills through credit cards by customers, etc.

3. Key Partners

Credit Card Issuers and Acquirers in India like different banks i.e. HDFC, ICICI, SBI, etc. have Payment Network Partners like VISA, MasterCard, etc. for processing the credit card transactions through them. Similarly, these credit card payment network companies mainly have 2 key partners i.e., Issuer Bank for distributing their credit card products to customers, and Acquirer banks for accepting and processing the information related to payment transactions that Merchants submit to them.

4. Key Resources

The main resources of Credit card companies are their customer service staff for providing fast and reliable assistance to all parties involved in the credit card payment process. Digital technology is also one of the key resources of these companies.

5. Key Activities

The key activity of Credit Card companies is to maintain platform management by providing a common platform between all parties i.e. customers, banks, and merchants. Other activities include transaction processing services, payment security activities, etc.

6. Channels

The major channels of Credit Card Companies include a website to market the products, services, and also advertisements through their own staff and television. Moreover, mobile apps are there for customers and companies organize different marketing campaigns like sponsored events, Trade shows, etc.

7. Customer Relationship

Following are the aspects through which it maintains great customer relationship.

- The credit card companies provide superior customer support by its offerings of different credit cards and benefits associated with them.

- To address any query of customers, 24/7 assistance is provided by the companies through toll-free numbers. Their customer care representatives are available to sort out any issues related to credit card services. Customer care service centres of these companies also assist in finding and applying for a credit card.

- Few credit card companies also provide missed call service facility to customers through which customers can view their credit card information by just giving a missed call from their registered contact number to the available numbers of the companies. For example, SBI is providing credit card missed call facility to its customers and by using this facility; customers can avoid the hassle of calling and keep on waiting for any customer care representatives to take their calls.

- SMS service is also available by the companies to address any credit card query of customers. One can use the above customer care facilities for various other purposes too, like card theft, card block, over usage of the card, etc.

- The credit card companies have Grievance Redressal cell that includes customer care representatives, complaint management team of expertise, Nodal officers, Customer service Managers, etc. to sort out any concern of the customer.

8. Cost Structure

Issuer or Issuing bank incurs various costs such as:

- Interest cost: Credit card issuing banks usually borrow the money that is required by the customers from different firms at quite low-interest rates. They further provide the borrowed amount at loan to customers at comparatively high-interest margins. For example, if an issuer bank charges 15% as the rate of interest from customers for lending money, and the bank has borrowed that money to lend at 5% interest rate, and if the balance remains with the customer for a whole year, then the issuer bank gets 10% as a profit or revenue on providing the loan. The difference of 5% is considered as interest expense. Most of the time banks don’t charge any interest if customers clear their bills of the credit card on time.

- Bad debts or charge offs: Few customers don’t pay their credit card bill ever, so some percentage of the total credit amount given to customers is considered as a loss to issuers.

- Rewards: Issuing banks have to provide different rewards to customers who use credit cards a lot. So, more the customers are given incentives, the more banks are liable to pay for providing these incentives.

- Operating expenses: Different operating costs like costs associated with printing the plastic of credit card, mailing bills and statements, marketing costs, the cost of maintaining a complete database of cardholders through computers, etc., are counted as an expense of the issuers.

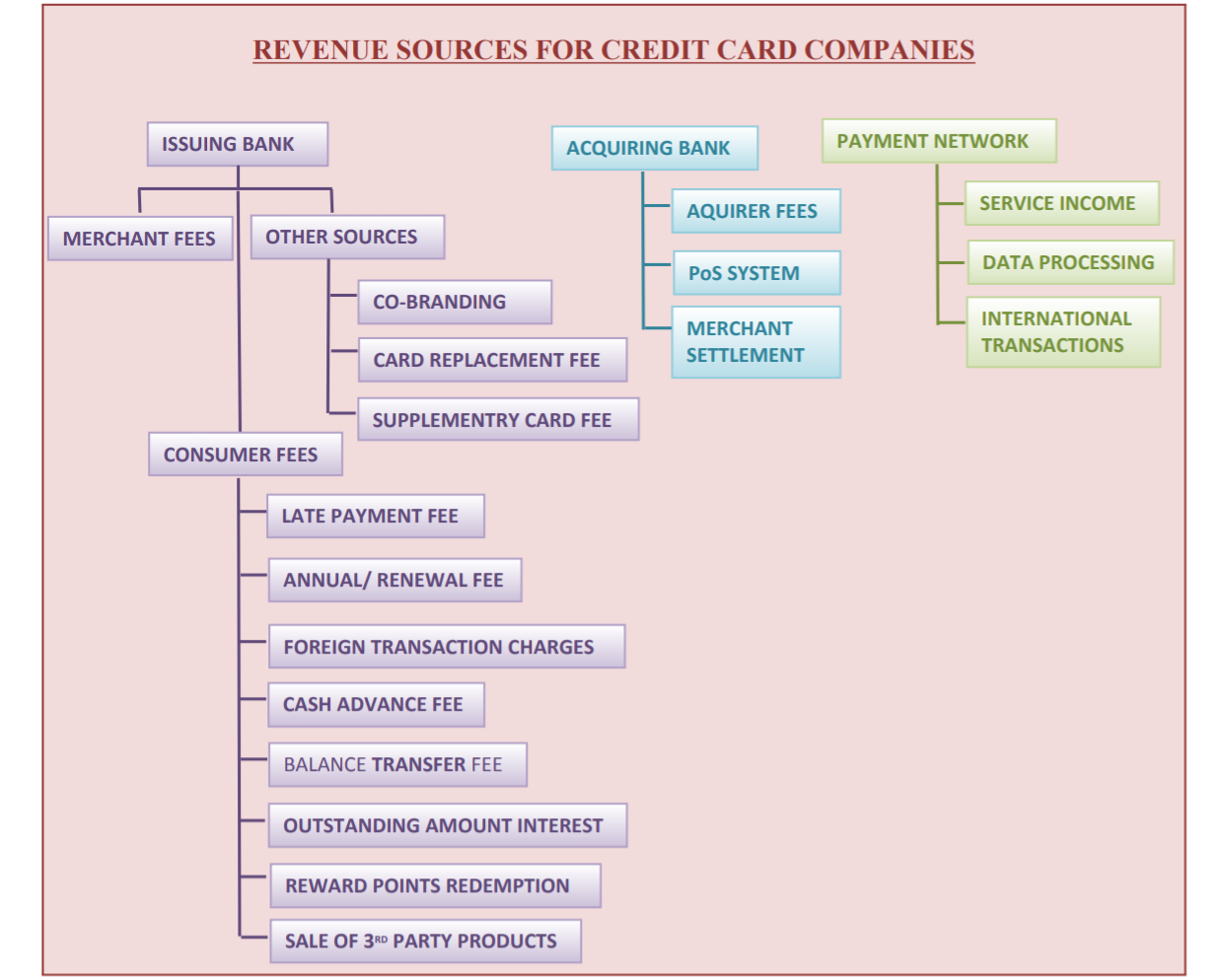

Revenue Streams of Credit Card Companies

Let’s explore different resources of Credit card companies through which they make money or profit:

Sources of revenue for Issuing bank (credit card Issuer)

- Interchange or Merchant Fees: It is assumed that while making payment through credit card by the cardholder; the retailer or Merchant gets the whole payment. However, whenever we use a credit card, a processing fee is paid by the merchant and is equals to a transaction’s percentage. Some portion of the fee is forwarded to the issuer or issuing bank through the payment network and referred to as interchange fees. This is generally around 1%-3% of the transaction. Payment networks set these fees and it varies as per the value and volume of transactions.

- Consumer Fees: Though credit card companies generate great revenue from merchant fees, they also earn money in the form of fee collection from the cardholders. This includes following fees:

- Fee for late payment and interest charges: Most of the credit cardholders don’t pay the complete bill of a credit card every month. This unpaid balance of credit card gives the occurrence of interest at defined rates. The majority of credit card customers are revolvers who act as the most profitable credit card customers for the issuing bank.

- Annual or renewal fees: Specific credit cards charge renewal fees annually and sign up fees. For example, the Platinum Travel credit card of American Express company which is considered as India’s one of the best premium travel credit card; has both joining fees and annual fee i.e. Rs. 35,00/- and Rs. 5000/- subsequently.

- Charges on foreign transactions: While purchasing anything from other than the home country, certain transaction rate is charged on the credit card at currency’s certain conversation rate and credit card account is levied by the charges of foreign currency conversion rate.

- Fees for cash advance: The credit card companies allow its users to withdraw certain cash against a predefined credit card limit. This is useful in emergency cash requirements as a loan for a short-term basis. The issuing bank charges this type of fee once customers utilize their credit card to withdraw cash through ATM. The Issuing bank charges both a transaction fee and an interest rate on this facility.

- Fees for balance transfers: While transferring debt between two credit cards (i.e. from one card to another) for availing the benefit of a lower rate of interest, customers are usually charged a certain percent of fee of the transferring amount. Though a few credit card issuing banks doesn’t charge this type of fee or may waive off for a particular period.

- Interest for converting outstanding amount: Most banks provide their credit card customers an option for converting the outstanding amount to easy EMIs. Banks charge specific interest for this.

- Revenue from the redemption of reward points: A little fee is charged by the issuing banks for making payment of any purchase with the customer’s reward points.

- Commission earned from the sale of 3rd party products: Sales agent who approaches customers for selling credit cards of a particular issuer may also look for cross-selling other products like mutual funds or investment schemes. Through the sale of such 3rd party products, a commission is earned by the business of credit card line.

Other Sources of Revenue

These are the other sources of revenue of credit card companies.

- Co-branding activities: The customers receive credit card statements in electronic form or at their mailing address that include advertisements of 3rd parties including their names. For this, credit card issuers or credit card companies take charges or fees from these advertisers.

- Card replacement fees

- Fees charged for supplementary card

Sources of Revenue for an Acquiring Bank

- Acquirer fees: The acquirer or acquiring bank processes a Merchant’s daily transactions of credit card and further those transactions are settled out by the bank with the issuer of the credit card. For this payment processing services on credit card transactions, acquirer deducts discount fees or charges commission from the MDR (Merchant discount rate).

- PoS Systems (TDR- Transaction discounting rate): PoS stand for Point of Sale; are the machines that facilitate card swipe at the time of a sale. Merchants, who are willing to take this service for customers, purchase the PoS systems by paying onetime fee. After that, the charges are based upon per transaction and are shared between card Issuer, Network, and Acquirer.

- Interest earned by Merchant settlement cycle: The acquirer or acquiring bank settles all transactions happen at the PoS of Merchant at regular intervals. Acquiring bank invests the money that resides with it for a time period, in bonds or investments for short-term to earn interest money from it.

Sources of Revenue for a Card Payment Network

- Revenue from service: Payment Network Company provides the support services to their financial institution clients for delivering their payment products and services to customers. They get revenue for providing such support services.

- Revenue from data processing: This includes money earned for clearing, network access, authorization, settlement, and other support, maintenance services that support processing of information and transaction.

- Revenue from International transactions: The revenue is also earned from the activities related to currency conversation and cross-border processing of transactions. These are mainly earned through cash volume and cross-border payments.

So, we can say that all the main three parties involved in credit card processing i.e. Issuer, Payment Network, and Acquirer earn money for every transaction. In a few cases, both Acquirer and Issuer are the same parties or Bank. Like in the case of American Express Company, all the 3 parties are the brand itself.

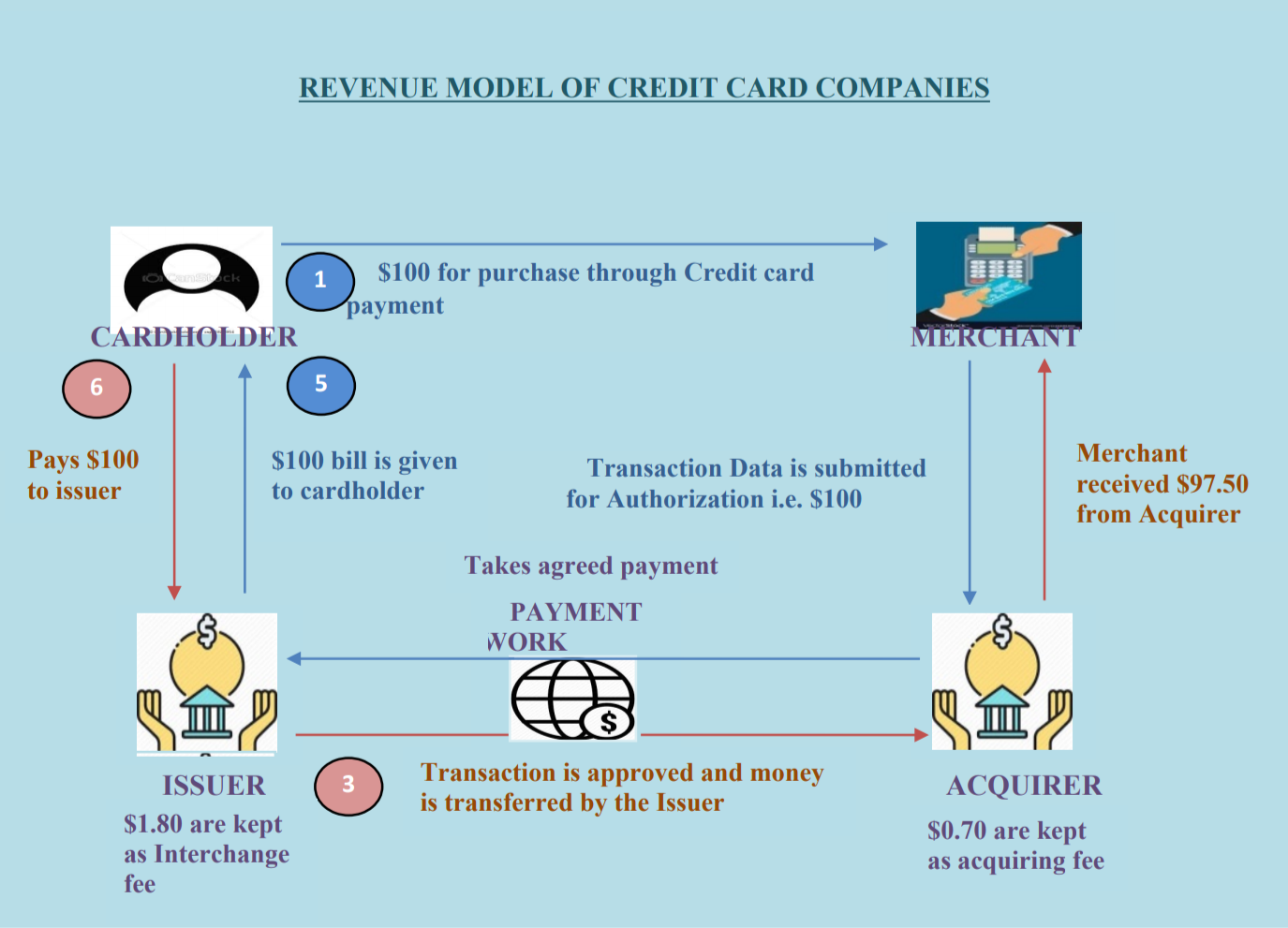

Revenue Model of Credit Card Companies

To understand the above revenue model of Credit Card Companies, let’s take an example:

- A cardholder makes payment of $100 to Merchant for the purchase of an Air conditioner through card swipe at the payment terminal.

- Suppose the Merchant Discount Fee (MDR) is $2.50 then the Merchant will receive $97.50 from Acquiring Bank for the transaction. This $2.50 would be distributed among the acquirer and issuer based upon the interchange fee. If this interchange rate is 1.8%, then $1.80 will go into the issuer’s account and the remaining $0.70 will be taken by the acquirer. The reason behind the more fee is kept by the issuer, is due to the more risk of payment default by the cardholder.

- The full amount of transaction i.e. $100 is collected by Issuing bank from the Cardholder. An agreed payment is made to Payment Network like VISA, MasterCard, etc. by Acquirer and Issuing bank.

- All the above parties in this revenue model are beneficiaries. Cardholder gets benefit due to safety, convenience, and rewards through card payments. Merchant gets the advantage of increased sales as they offer payment options to customers. Banks increase their revenue by payment interests, card fees, etc. Payment Network earns revenue through transaction processing, payment volumes, and value-added services.

My brother recommended I might like this website. He was entirely right. This post actually made my day. You cann’t imagine just how much time I had spent for this information! Thanks!