Revenue recognition determines the specific condition when the revenue can be realized. Revenue is recognized when it is realized or realizable and is earned (usually when goods are transferred or services rendered.) Revenue is at the heart of all business performance, everything hinges on the sale. As such, regulator knows how tempting it is for companies to push the limits on what qualifies as revenue, especially when not all revenue is collected when the work is completed. The revenue is recognized when the delivery of promised goods or services matches the amount expected by the company in exchange for the goods or services. There are mainly five different types of methods by which revenue can be recognized.

1. Sales Basis Method

Under the sales basis method, revenue can be recognized at the moment the sale is made, or when the product is delivered to the customer or services are rendered. This occurs even if cash was received prior to contractual fulfillment. For example, if a customer purchases an annual Netflix subscription for Rs. 1200, the revenue of only Rs. 100 can be recognized every month.

Revenue Recognition sales method

2. Installment method for revenue recognition

The installment method is the key term for this revenue recognition. If a company is concerned with the customer’s ability to pay, then this method comes into play. The installment method is usually preferred for high-value purchases. Such as vehicles, real estate, and heavy electric appliances. For example, if a car is purchased for Rs. 5 lakh, and the customer pays Rs. 1 lakh down payment with a monthly installment of Rs. 40,000. Now, at the time of sale, the company will recognize Rs. 1,00,000 once the vehicle is transferred to the customer, and Rs. 40,000 every month after receiving the monthly installment.

Installment method for revenue recognition

3. Percentage of completion

Companies engaged in long-term projects usually prefer the percentage of completion method for revenue recognition. This method allows companies to recognize revenue according to milestones or other indicators of progress. The percentage of completion method allows the company to recognize revenue closer to real-time, rather than waiting until the end of a lengthy contract. For example, if you own a house construction company that contracts to build a house for a total of Rs. 40,00,000 then the contract can be written so that you can recognize Rs. 10,00,000 for every 25% of house completion.

4. Completed contract method

When the requirement of completion percentage can’t be estimated or the contract isn’t enforceable, then the completed contract method is used for revenue recognition. The completed contract method allows companies to recognize revenue when the entire contract is fulfilled, and when all performance obligations have been satisfied. For example, a mobile company gets an order for three shipments of 300 mobile each in three consecutive quarters. The term of the contract won’t be met until the third or final shipment of 300 mobiles. So, revenue can’t be recognized until that time.

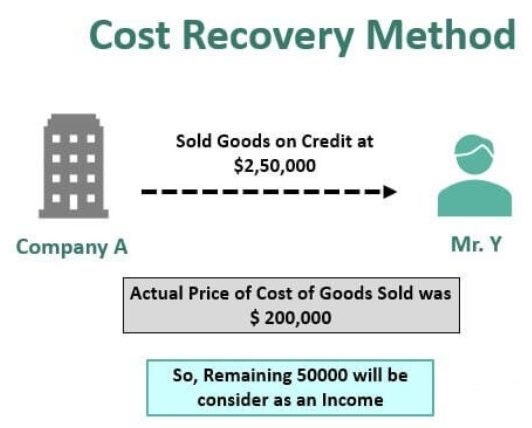

5. Cost recoverability method

Under this method, which is considered the most conservative revenue recognition method, you can recognize revenue only after you have recouped all the costs associated with the contract. This is mostly used when the company can’t reasonably estimate the total expenses required to complete a project. Revenue can only be recognized once all expenses are incurred or accounted for. For example, if a software program is created for a total cost of Rs. 10,00,000, and the software license is later available to other companies for Rs. 3,00,000 in the first quarter then Rs. 3,00,000 would serve as an offset to Rs. 10,00,000.

Finding the right revenue recognition method

Every method discussed above as well as other available methods have both pros and cons. Regardless of your business model, the most suitable revenue recognition is one of the most critical tasks your financial team undertakes. From product inception through revenue recognition, you need a system that empowers you to monetize any revenue opportunity. Revenue recognition doesn’t just cover how you record revenue, but how you account for the cost involved in obtaining a contract (like sales, commissions) and fulfilling a contract (like labor, material, PPP, etc.).