Revenue recognition in construction is the reporting of revenue and profits by construction companies in their financial statements. Revenue recognition in construction is a challenging and complex process as construction contracts are mostly long-term and complex.

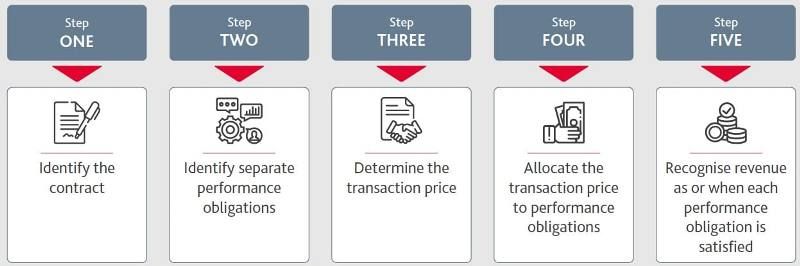

Five Steps of Revenue Recognition

According to the Accounting Standards Codification (ASC) 606 and IFRS 15 standards, there are five steps to recognize revenue:

1. Identify the contract with a customer

A contract (whether written or oral) with a customer should be legally enforceable and certain criteria should be met, for example, rights to goods or services and payment terms should be clearly defined, it should have commercial substance, it should be approved, and parties should be committed to their obligations.

2. Identify separate performance obligations

Distinct promises mentioned in a contract are called performance obligations. The IFRS 15 standard says that the revenue should be counted separately for every performance obligation when these obligations are accomplished.

3. Determine the transaction price

The transaction price is the expected amount for promised goods/services to the customer. Sometimes the transaction price is variable and sometimes fixed. Variable amounts of consideration include discounts, rebates, refunds, credits, concessions, incentives, performance bonuses, penalties, and contingent payments.

4. Allocate the transaction price to performance obligations

The transaction price should be allocated to every performance obligation including discounts and freebies.

5. Recognise revenue when each performance obligation is satisfied

According to this standard, the revenue is recognized only after each performance obligation is satisfied mentioned in the contract.

Examples

Cash Basis

According to this method, construction companies recognize revenues when cash is received regardless of when the services are actually performed. This method is usually followed by small and medium-sized construction companies.

Accrual Basis

Under this method, construction companies record revenue and expenses during the work is performed regardless of when the cash is actually received.

Percentage-of-Completion Method

Under this method, revenue is recognized over the period of the construction work. This is done by calculating the percentage of completion based on the costs incurred to date relative to the total estimated contract costs. Under this method, revenue could be reported more evenly throughout the project.

Completed Contract Method

Under this method, revenue is recognized only after the entire contract is completed and all performance obligations are satisfied.