IFRS 15 is an International Financial Reporting Standard (IFRS) that was adopted in 2014 and implemented in 2018. IFRS 15 was developed as a joint project of the International Accounting Standards Board (IASB) and the Financial Accounting Standards Board (FASB). The standard is a guide about when and how to recognize revenue from contracts with customers. Before IFRS 15, many standards existed including IAS 18, IAS 11, SIC 31, IFRIC 13, IFRIC 15, and IFRIC 18.

IFRS 15: Five-step Revenue Model

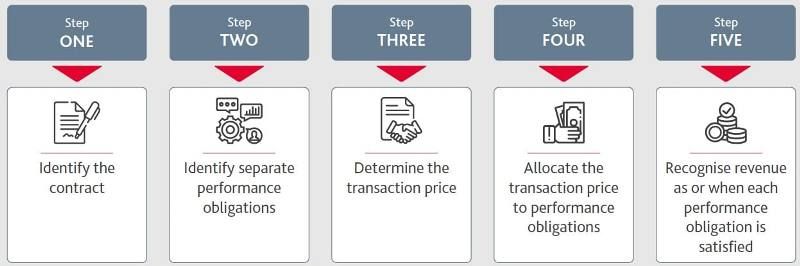

The IFRS 15 revenue model is discussed in five steps:

1. Identify the contract with a customer

A contract (whether written or oral) with a customer should be legally enforceable and certain criteria should be met, for example, rights to goods or services and payment terms should be clearly defined, it should have commercial substance, it should be approved, and parties should be committed to their obligations.

2. Identify separate performance obligations

Distinct promises mentioned in a contract are called performance obligations, for example, if a car seller has a contract with a customer in which the seller mentions that apart from selling the car to the customer, the seller will also give three years of maintenance service to the customer, then the contract will have two distinct performance obligations – delivery of the car to the customer, and three years of maintenance service. The IFRS 15 standard says that the revenue should be counted separately for both performance obligations when these obligations are accomplished.

3. Determine the transaction price

The transaction price is the expected amount for promised goods/services to the customer. Sometimes the transaction price is variable and sometimes fixed. Variable amounts of consideration include discounts, rebates, refunds, credits, concessions, incentives, performance bonuses, penalties, and contingent payments.

4. Allocate the transaction price to performance obligations

Allocation of transaction price to performance obligations may include discounts and freebies. For example, if a pair of shoes costs Rs. 100 to the customer, and the seller promises to give a pair of shocks free to the customer along with a pair of shoes, then the seller can not allocate the transaction price only to the pair of shoes, and it should also allocate the transaction price to the pair of shocks, which, for example, may cost Rs. 20. In this case, the allocation of the transaction price to performance obligations can be determined in the following manner:

Cost of a pair of shoes = Rs. 100

Cost of a pair of shocks = Rs. 20

Allocation of transaction price for the pair of shoes = Rs. 100/120*100 = Rs. 83

Allocation of the transaction price for the pair of shocks – Rs. 20/120*100 = Rs. 17

5. Recognise revenue when each performance obligation is satisfied

According to this standard, the revenue is recognized only after each performance obligation is satisfied mentioned in the contract. The revenue may be recognized over time, for example, long-term contracts like the construction of a bridge or dam, or it can be recognized at a point in time, for example, short-term contracts like the instant delivery of goods/services.

IFRS 15 Illustrative Examples

1. Software Sales

A software company signs a contract with a client to sell software licenses. In the contract, the company also mentions that it would provide maintenance for three years. Now, there are two performance obligations – providing software licenses and providing maintenance for three years. In this case, the allocated transaction price must be determined for each performance obligation, and the revenue should only be recognized after the customer receives the license, and the three years of maintenance service is completed.

2. Construction Contracts

A construction firm signs a contract to build a commercial building. The construction company promises to construct the building, and it also promises to comply with regulatory standards. Now, there are two performance obligations – construction of the building, and regulatory compliance. In this case, the allocated transaction price must be determined for each performance obligation, and the revenue should only be recognized after the entire construction work is completed, and regulatory compliance is satisfied.

3. Subscription Services

A streaming service signs a contract with a customer for a monthly subscription. The streaming service promises to provide access to the streaming service, and it also offers customer support to the customer. Now, there are two performance obligations – providing the streaming service, and customer support. In this case, the allocated transaction price must be determined for each performance obligation, and the revenue should only be recognized after the customer receives the streaming service, and the customer support promise is satisfied.

4. Telecommunications

A telecom company sells a smartphone with a two-year service contract. There are two performance obligations – the sale of the phone, and providing telecom services. Now, the allocated transaction price must be determined for each performance obligation, and the revenue should only be recognized after the smartphone is delivered to the customer, and the two-year service contract is fulfilled.

5. Manufacturing

A manufacturing company sells customized machinery, and it also promises to provide training to handle the machinery. There are two performance obligations – producing and delivering the machinery, and providing training. Now, the allocated transaction price must be determined for each performance obligation, and the revenue should only be recognized after the machinery is delivered to the customer, and the training is completely provided as promised in the contract.

6. Consulting Services

A consulting firm signs a contract with a customer to provide advisory services, and it also promises to provide a final report at the end of the service. There are two performance obligations, providing consulting services, and delivering a final report. Now, the allocated transaction price must be determined for each performance obligation, and the revenue should only be recognized after the customer receives the advisory services along with the final report.

7. Retail Sales

A retail store sells electronic gadgets with an extended warranty. There are two performance obligations, selling the gadget, and providing the extended warranty. Now, the allocated transaction price must be determined for each performance obligation, and the revenue should only be recognized after the electronic gadget is delivered to the customer, and the extended warranty is fulfilled.

8. Real Estate Sales

A real estate developer sells residential properties and also promises to provide post-sale support. Two performance obligations are there – selling the property and providing post-sale support. Now, the allocated transaction price must be determined for each performance obligation, and the revenue should only be recognized after the residential property is sold to the customer, and the post-sale support is completely satisfied as promised in the contract.

9. Advertising Services

An advertising agency signs a contract with a client to provide advertising services and also promises to provide a campaign report. There are two performance obligations – providing advertising services and delivering campaign reports. Now, the allocated transaction price must be determined for each performance obligation, and the revenue should only be recognized after the advertising services are completely provided to the client along with the campaign report.

10. Licensing Agreements

A media company licenses its content to a streaming platform and also promises to provide technical support. There are two performance obligations – granting content licensing rights and providing technical support. Now, the allocated transaction price must be determined for each performance obligation, and the revenue should only be recognized after the content is provided to the streaming platform, and the technical support is completely fulfilled as promised in the contract.